Diamond Capital Management's Market Commentary

July, 2026

Jeff C. Mantock, CFA, CMT

Vice President, Chief Investment Officer and Manager

Executive Summary:

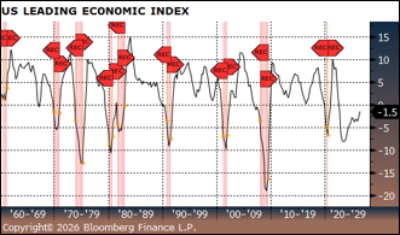

- With no recession in sight, the bull market should remain intact. We would continue to view pullbacks in stocks as likely buying opportunities.

- Equity valuations are modestly elevated but reasonable given the current backdrop of earnings growth, steady economic conditions, and continued investor demand for growth-oriented sectors.

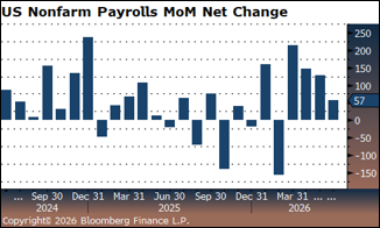

- Lower inflationary pressures and the weaker jobs report in June will likely keep the Federal Reserve on the sidelines for the foreseeable future.

|

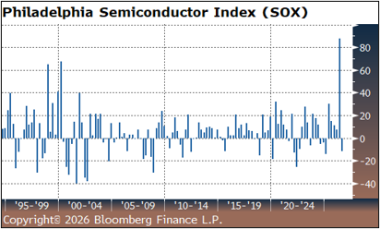

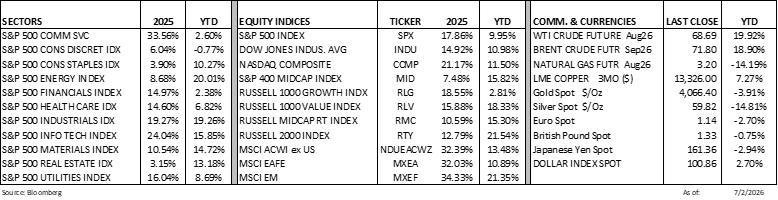

Equity markets ended the first half of 2026 on a strong footing, supported by improving earnings expectations and renewed investor enthusiasm surrounding artificial intelligence. Most major equity indices delivered solid gains, with several posting double-digit returns. Year to date, the S&P 500 Index has outperformed on an equal-weighted basis relative to its market-cap-weighted counterpart, suggesting broader participation beyond the largest constituents. Within the “Magnificent Seven,” Alphabet was the strongest performer, while Meta Platforms, Inc. was the most notable laggard. Inflows into AI- and technology-focused equity funds reached a record pace, and although chip stocks have pulled back thus far in July, semiconductors just completed their strongest quarter on record.

|

|

U.S. large-cap equity valuations remain modestly elevated. As of July 2, 2026, the S&P 500 Index traded at a forward price-to-earnings ratio of 20.9x, above its 10-year and 15-year averages of 19.8x and 17.6x, respectively. This premium reflects the post-pandemic re-rating of equities, driven largely by mega-cap technology and AI-related companies. While higher interest rates or discount rates could make these valuations more difficult to sustain, we believe continued growth in corporate earnings should provide meaningful support.

|

|

|

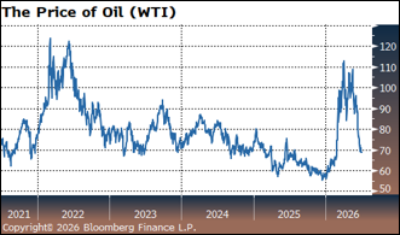

We remain constructive on the financial markets and continue to favor equities. With no recession presently in sight, we believe that pullbacks in stocks are likely to present attractive long-term buying opportunities. Inflation risks have also moderated in recent weeks, helped by lower oil prices, while the latest jobs report supports the case that the Federal Reserve is unlikely to raise rates in the near term. At the same time, investor concern about missing further upside in the ongoing rally could provide additional support for equity prices.

Happy 250th Birthday America!

|

|

The information and material contained herein is provided solely for general information purposes. This material is not intended to be investment advice nor is this information intended as an offer or solicitation for the purchase or sale of any security or other financial instrument. Any opinions expressed herein are given in good faith, are subject to change without notice, and are only current as of the stated date of their issue. Certain sections of this publication contain forward-looking statements that are based on the reasonable expectations, estimates, projections, and assumptions of the authors, but forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Investment ideas and strategies presented may not be suitable for all investors. No responsibility or liability is assumed by The National Bank of Indianapolis, or its affiliates for any loss that may directly or indirectly result from use of information, commentary, or opinions in this publication by you or any other person.

Learn more about Diamond Capital Management services from The National Bank of Indianapolis: